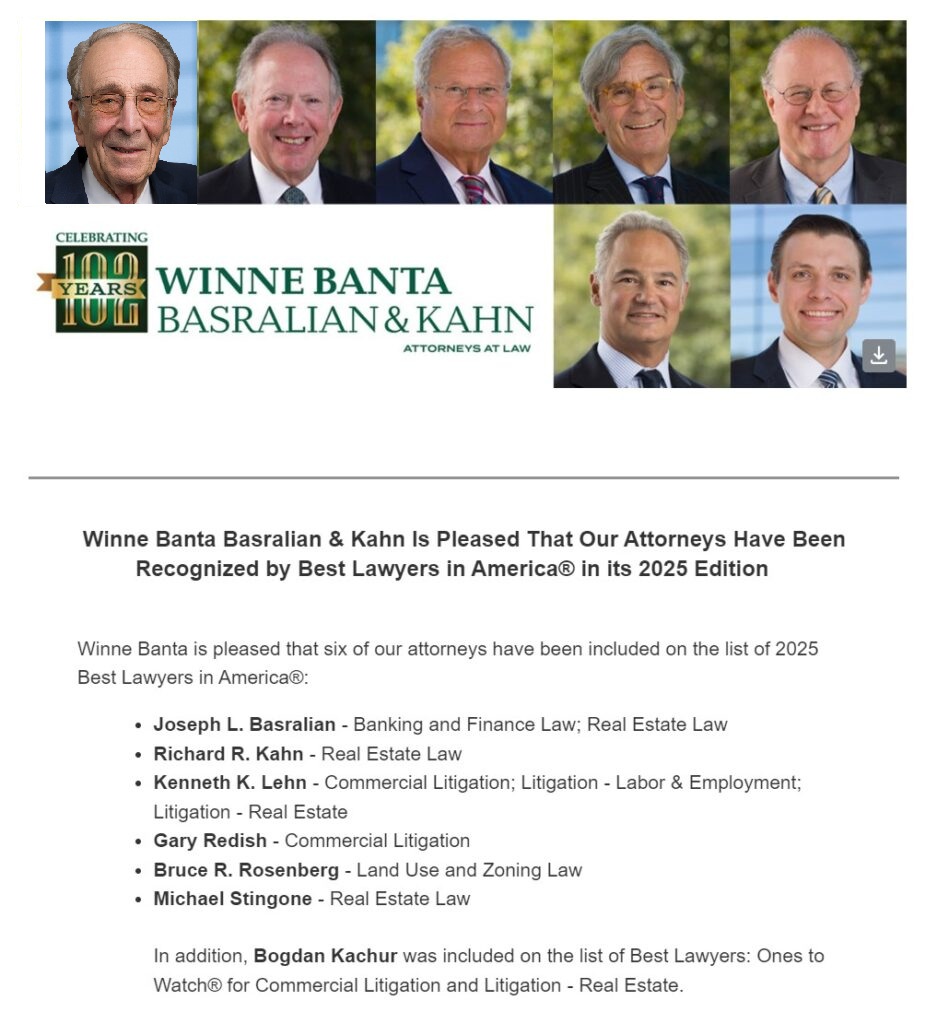

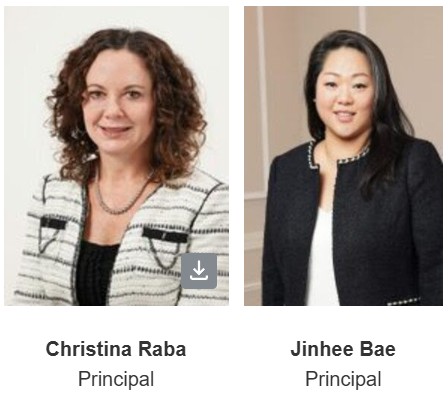

Power Law Firms Joins Winne Banta

We’re pleased to announce that Christine Raba and Jinhee Bae, principals of Power Law Firm LLP, are joining the firm.

A Hackensack-based practice concentrating in trusts, estates, and elder law, led by members Christine Raba and Jinhee Bae, brings dedicated depth that expands Winne Banta’s elder law and special needs planning services while complementing the trusts and estates practice the firm’s clients have long relied on.

Raba’s and Bae’s practice focuses on tax-efficient family wealth transfers, asset protection, and special needs planning.

Raba and Bae join Winne Banta as principals, bringing their team and focused experience to the firm’s established tax and trust and estate practices, giving current and future clients access to a broader, full-service platform for planning that spans generations, all under one roof.

“I have long admired the work Christine, Jinhee, and their team have done at Power Law Firm, and we are thrilled to welcome them to Winne Banta,” said Joseph L. Basralian, president of Winne Banta. “Their elder law and special needs experience allows us to offer even more to the individuals and families we serve. It means our clients, and the clients who will come to us in the years ahead, have trusted guidance for some of life’s most important and sensitive planning decisions.”

With the addition, Winne Banta clients now have a single destination for estate planning, trust and estate administration, elder law, special needs planning, and asset protection, complementing the firm’s established strengths in litigation, finance and corporate services, real estate, land use and zoning, and tax.

Power Law Firms Joins Winne Banta Read More »